A Guide to Kenya's Social Health Authority (SHA): What the NHIF Transition Means for Your Payslip and Your Health

You open your payslip, maybe with a quick glance, maybe with the detailed focus of a forensic accountant. You scan past the familiar lines—basic salary, PAYE, NSSF—and then you see it. A new deduction, larger than the old NHIF amount, labeled "SHA Contribution."

Your first thought is likely a simple one: What is this? And why is it more?

It’s not just you. Across Kenya, salaried professionals are having this exact moment. The National Health Insurance Fund (NHIF), a fixture of Kenyan employment for decades, is gone. In its place is the Social Health Authority (SHA), a new body established by the Social Health Act, 2023.

This isn't just a name change. It's a fundamental overhaul of how public health insurance is funded and delivered in Kenya. It changes how much you contribute, how you access care, and what benefits you're entitled to.

If you're a busy professional who just wants to understand the bottom line, you're in the right place. This is your no-nonsense guide to the new SHA, what it means for your wallet, and how it compares to the system you knew.

Table of Contents

- NHIF vs. SHA: A Head-to-Head Comparison

- Your New Payslip: Understanding SHA Contributions for Employed Kenyans

- Where Your Money Goes: A Simple Guide to the Three SHA Funds

- The Big Question: Do I Still Need Private Health Insurance?

- Your Next Steps

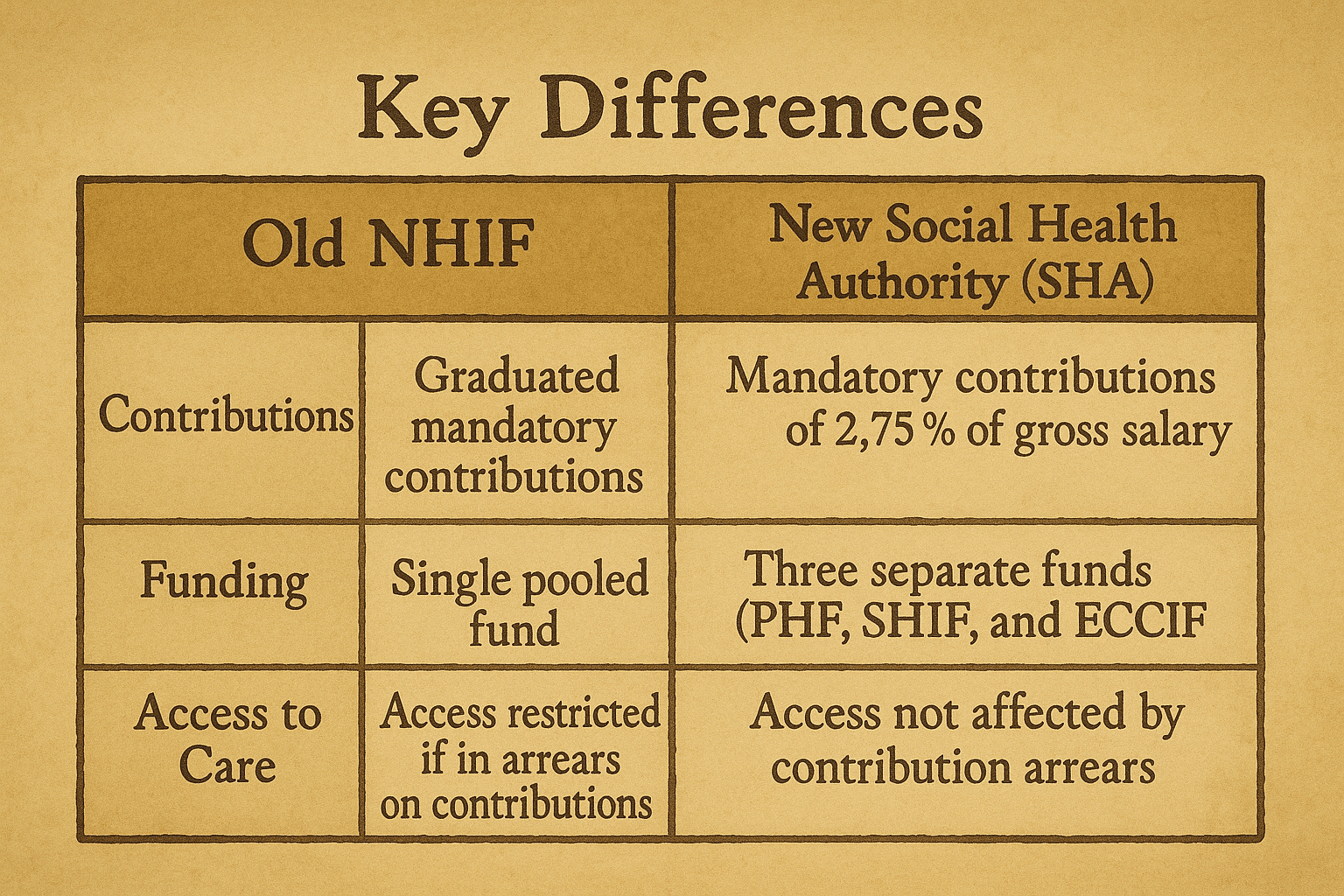

NHIF vs. SHA: A Head-to-Head Comparison

To understand where we're going, we first need to be clear about where we've been. The NHIF had become a household name, but it faced significant challenges, including financial unsustainability and unequal benefit distribution. The government's push for Universal Health Coverage (UHC) prompted a complete redesign.

The Social Health Authority (SHA) is the result. It's structured differently, funded differently, and promises to deliver care differently.

Here’s a direct comparison of the key features:

| Feature | Old System: NHIF | New System: Social Health Authority (SHA) |

|---|---|---|

| Governing Law | NHIF Act, 1998 | Social Health Act, 2023 |

| Contribution Model | Graduated fixed amount. Ranged from Ksh 150 to a maximum of Ksh 1,700 per month for salaried employees. A flat Ksh 500 for the self-employed. | Percentage of income. A mandatory 2.75% of the gross monthly household income. |

| Contribution Floor | Ksh 150 for those earning Ksh 5,999 or less. | Ksh 300 per month for households with no income. |

| Contribution Cap | Ksh 1,700 for those earning Ksh 100,000 or more. | No cap. A Ksh 5,000 cap was proposed in early drafts but not adopted — the 2.75% applies with no upper ceiling. |

| Funding Structure | A single fund that covered all benefits, from outpatient to inpatient. | **Three distinct funds:**1. Primary Healthcare Fund (PHF)2. Social Health Insurance Fund (SHIF)3. Emergency, Chronic, and Critical Illness Fund (ECCIF) |

| Access to Care | Members could often go directly to an accredited hospital of their choice for many services. | A primary care-first model. Members must first seek services at a Level 2 or 3 facility (dispensary or health center). A referral is needed for higher-level care. |

| Benefit Scope | Covered a range of services but had well-known limits, especially for chronic and critical illnesses. | Designed to be more comprehensive. The three-fund system separates funding for primary care, secondary/tertiary care, and catastrophic illnesses. |

| Registration | Mandatory for all Kenyans over 18, but enforcement varied. | Mandatory for all residents of Kenya. Registration is linked to accessing government services, similar to the KRA PIN. |

The takeaway is clear: the SHA is a more ambitious, and for many, a more expensive system. The core idea is to create a larger, more equitable pool of funds to provide a wider safety net for everyone.

Your New Payslip: Understanding SHA Contributions for Employed Kenyans

The most immediate change for any salaried person is the new deduction. The old Ksh 1,700 cap was a predictable, if sometimes frustrating, ceiling. The new 2.75% of gross salary model changes the calculation entirely.

Let's break that down.

What is "Gross Salary?"

This is a critical point. The 2.75% is calculated on your gross monthly income. That means your total earnings before any other deductions like PAYE, NSSF, HELB, or pension contributions are taken out.

For example, if your payslip shows:

- Basic Salary: Ksh 90,000

- House Allowance: Ksh 30,000

- Commuter Allowance: Ksh 10,000

Your Gross Salary is Ksh 130,000. This is the figure the 2.75% applies to.

Worked Examples:

Let's see how this plays out at different income levels compared to the old NHIF system.

- Scenario 1: Junior Professional

- Gross Salary: Ksh 60,000

- Old NHIF Contribution: Ksh 1,300

- New SHA Contribution (2.75% of 60,000): Ksh 1,650

- Difference: +Ksh 350 per month

- Scenario 2: Mid-Level Manager

- Gross Salary: Ksh 150,000

- Old NHIF Contribution: Ksh 1,700 (the maximum)

- New SHA Contribution (2.75% of 150,000): Ksh 4,125

- Difference: +Ksh 2,425 per month

- Scenario 3: Senior Executive

- Gross Salary: Ksh 400,000

- Old NHIF Contribution: Ksh 1,700 (the maximum)

- New SHA Contribution (2.75% of 400,000): Ksh 11,000 — there is no cap, so the full 2.75% applies no matter how high the salary.

- Difference: +Ksh 9,300 per month

As you can see, higher earners will see a significantly larger deduction from their monthly pay. This progressive model is designed to have those with greater means contribute more to the national health pool, a common feature of social insurance systems worldwide.

What About the Minimum and Maximum?

The Social Health Act, 2023, establishes a floor for contributions — but, unlike the old NHIF, no ceiling — so the lowest earners are protected while higher earners pay proportionally.

- Minimum Contribution: For households with no formal income (the unemployed or vulnerable), the minimum contribution is set at Ksh 300 per month.

- Maximum Contribution: There is no maximum. A cap of Ksh 5,000 per month was floated in early draft regulations but was not adopted, so the 2.75% applies to your full gross salary no matter how high it is — only the Ksh 300 minimum applies at the bottom end.

Where Your Money Goes: A Simple Guide to the Three SHA Funds

So, you're paying more. The natural next question is, "What am I getting for it?"

Under the SHA, your 2.75% contribution isn't just thrown into one big pot like with NHIF. It's strategically divided to serve different purposes across three new, specialized funds. Understanding these is key to understanding the value of the new system.

1. The Primary Healthcare Fund (PHF)

- What it is: This fund is designed to cover the cost of basic, everyday healthcare at the grassroots level.

- How it works: It pays for services at public Level 2 (dispensaries) and Level 3 (health centers) facilities. When you register for SHA, you will be linked to a specific local facility. The goal is to make essential services available to you for free at the point of care, without you needing to pay anything out of pocket.

- What it covers: Think of this as your first stop for healthcare. Services include:

- Outpatient consultations for common illnesses.

- Child welfare clinics (immunizations).

- Maternity services (antenatal and postnatal care).

- Health and wellness promotion.

- Screening for common conditions.

The big idea here is "preventive care." By encouraging people to deal with small health issues early and for free, the system hopes to prevent them from becoming bigger, more expensive problems later on.

2. The Social Health Insurance Fund (SHIF)

- What it is: This is the main insurance fund, the true successor to the old NHIF system. It's designed to cover more complex and expensive treatments that require hospitalization or specialists.

- How it works: To access this fund, you will generally need a referral from your designated primary care facility (covered by the PHF). This "gatekeeper" model is designed to ensure that hospital resources are used for cases that genuinely need them.

- What it covers: This is the fund you'll rely on for more serious medical events. It covers services at Level 4, 5, and 6 hospitals (from county hospitals to national referral hospitals), both public and private, as long as they are accredited by the SHA. Key benefits include:

- Inpatient services (hospital stays).

- Outpatient services at higher-level facilities.

- Surgical procedures.

- Maternity and childbirth services at hospitals.

- Diagnostic imaging (MRIs, CT scans).

- Specialist consultations.

This is the core of your health insurance, protecting you from the significant costs associated with hospital-based care.

3. The Emergency, Chronic, and Critical Illness Fund (ECCIF)

- What it is: This is the national safety net for financially catastrophic health events. It's specifically set aside to cover the most expensive and long-term medical conditions that could ruin a family financially.

- How it works: This fund is accessed after the benefits from the Social Health Insurance Fund (SHIF) have been exhausted. It’s meant to provide a cushion for severe cases.

- What it covers: The fund is specifically for:

- Emergency Treatment: Covering costs for things like serious road accidents or other medical emergencies where immediate, life-saving care is needed.

- Chronic and Critical Illnesses: This includes long-term management of conditions like cancer, diabetes, kidney failure (including dialysis), and hypertension.

This fund directly addresses one of the biggest weaknesses of the old system, where patients with severe illnesses often hit their benefit limits quickly, forcing them to pay huge sums out of pocket.

The Big Question: Do I Still Need Private Health Insurance?

This is, perhaps, the most practical question for a salaried professional who may already have a private insurance plan through their employer or one they pay for themselves.

The answer is: It depends on your needs and expectations.

The Social Health Authority aims to provide a comprehensive package of essential health services for all Kenyans. For many, the SHA cover will be a significant improvement and may be sufficient for their needs.

However, private insurance can still play a crucial role as a supplementary cover. Here’s where it can add value:

- Wider Choice of Hospitals: While SHA will accredit a wide range of public and private facilities, your private insurance might give you access to a premium network of high-end private hospitals that may not be on the SHA panel, or it might cover services at those hospitals with fewer restrictions.

- Private Rooms and Enhanced Comfort: SHA coverage will likely be for general ward accommodation. If you prefer a private room during a hospital stay, private insurance is what will cover that.

- Covering Gaps and Limits: No public health system covers 100% of everything. There may be specific drugs, experimental treatments, or co-payments that the SHA does not cover. Private insurance can fill these gaps.

- Faster Access to Specialists (Potentially): The SHA's referral system is designed for efficiency, but in some cases, private insurance might offer a more direct or faster route to see a specialist of your choice without needing a referral from a primary care facility.

- Overseas Treatment: The SHA is designed for treatment within Kenya. If your needs include coverage for medical treatment abroad, private insurance is essential.

The Verdict: Think of SHA as your foundational health cover, your non-negotiable safety net. Think of private insurance as a "top-up" or an "enhancement" that buys you more choice, comfort, and coverage for benefits beyond the essential package. For many professionals, a combination of both will provide the most robust protection.

Your Next Steps

The transition from NHIF to SHA is a major policy shift, and it’s natural to have questions. But for now, the path forward is clear.

- Verify Your Contribution: On your next payslip, check the SHA deduction. Ensure it correctly reflects 2.75% of your gross monthly salary. If you have questions, the first point of contact should be your employer's HR or payroll department.

- Confirm Your Registration: The government is conducting a mass registration of all Kenyans into the new system. You can check your status and manage your dependents (spouse and children) through the official government platforms, typically integrated with e-Citizen.

- Know Your Primary Facility: Familiarize yourself with the Level 2 or 3 health facility you are assigned to. This is your new front door to the healthcare system for most non-emergency needs.

💡 The shift to the Social Health Authority is a bold step towards making quality healthcare accessible to all Kenyans. For the salaried professional, it demands a new understanding of your payslip and a slight adjustment in how you approach healthcare. By understanding the new contribution structure and the three-fund system, you can navigate this change with confidence, knowing exactly what your money is paying for: a more structured and comprehensive health cover for you and your family.

Ready to Get Started?

Get personalized advice and quotes tailored to your needs. No pressure, just honest guidance.

👉 Or start a chat with our assistant now.