The Ultimate Checklist: How to Choose Your First Medical Cover in Kenya for Under KES 2,500/Month

Let’s be real: health insurance in Kenya has a reputation for being expensive. Many young Kenyans assume it’s something you only start thinking about when you’ve “made it” — or when you start a family.

But here’s the truth: you don’t need 20K a month to get decent cover. With as little as KES 2,500/month, you can get a solid starter plan that protects you from the big shocks (and even some of the small ones).

The trick? Knowing what to look for — and what to avoid. That’s where this checklist comes in.

Table of Contents

- ✅ 1. Start with NHIF (SHA Now) — Your Non-Negotiable Base

- ✅ 2. Focus on Inpatient Cover First

- ✅ 3. Outpatient? Nice-to-Have, Not Must-Have (Yet)

- ✅ 4. Watch Out for Waiting Periods

- ✅ 5. Compare, Don’t Assume

- ✅ 6. Keep It Alive — Never Miss a Payment

- Example: The 28-Year-Old Freelancer in Nairobi

- Conclusion: Peace of Mind Doesn’t Need to Be Expensive

✅ 1. Start with NHIF (SHA Now) — Your Non-Negotiable Base

- Cost: 2.75% of gross income (minimum KES 300, no upper cap).

- Why it matters: It’s mandatory, but also a safety net for public hospitals. Think of it as ugali — the base of your meal.

- Pro Tip: Don’t skip this. Even if you only use private insurance, SHA is still your fallback in government facilities.

✅ 2. Focus on Inpatient Cover First

When you’re on a tight budget, inpatient cover (hospital admissions) is the most important.

- Look for a plan with at least KES 1–2M inpatient limit.

- Confirm which hospitals are in the network — otherwise you’ll be stuck paying cash at the door.

- Skip the fancy extras for now (like optical or dental).

💡 Rule of thumb: One serious admission at a private hospital can cost KES 300K+. Don’t risk it.

✅ 3. Outpatient? Nice-to-Have, Not Must-Have (Yet)

Outpatient is great — it covers clinics, labs, scans, meds. But under 2,500/month, most budget plans won’t give you a high limit.

- If you rarely visit doctors, you can skip outpatient in your first year.

- Instead, put that extra cash into a small emergency fund (even 500 bob a month helps).

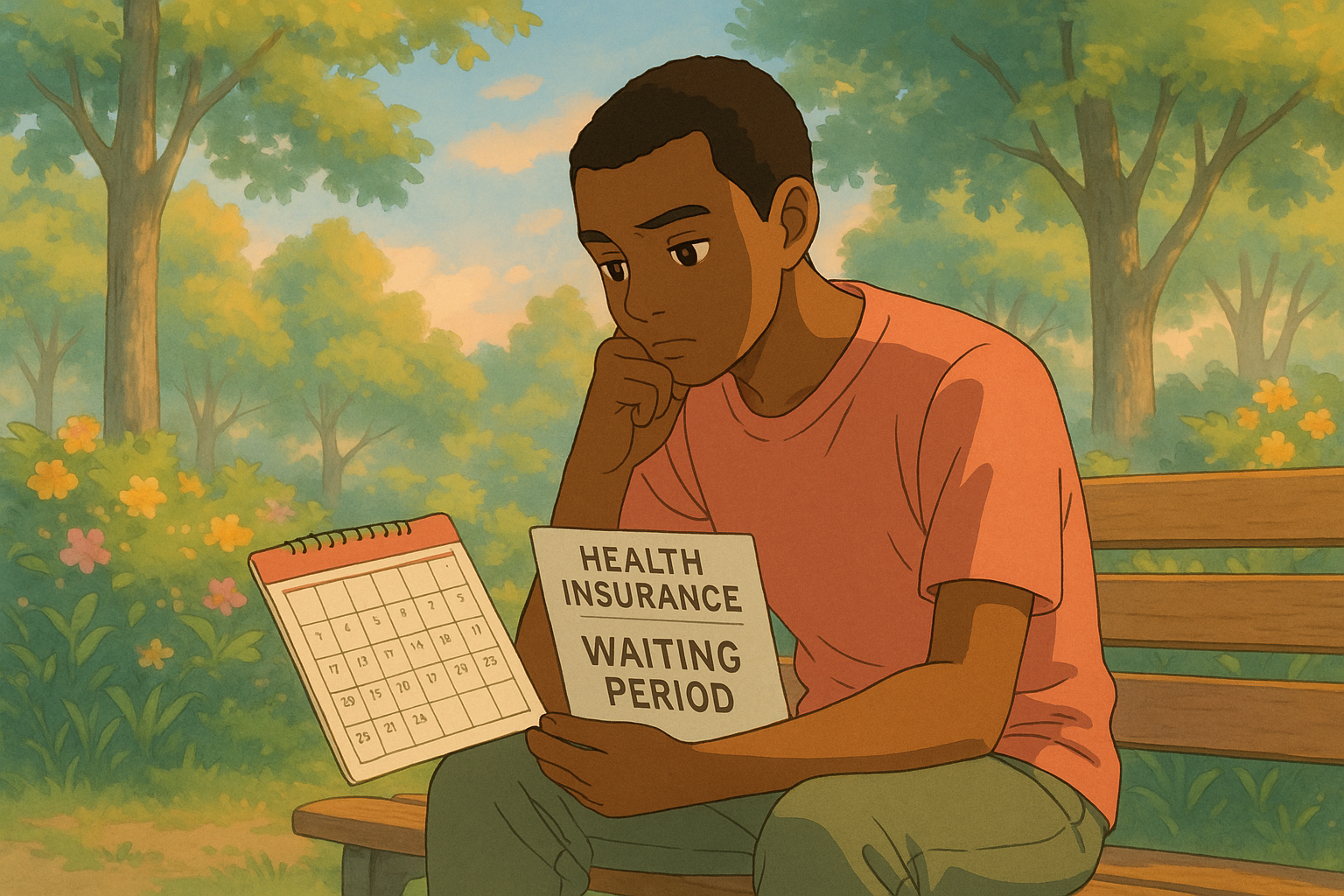

✅ 4. Watch Out for Waiting Periods

This is the classic newbie trap.

- General Illness: Usually 30 days.

- Maternity: 10–12 months.

- Chronic conditions / surgeries: 1–2 years.

👉 Don’t wait until you need the cover to buy it. Buy it now, so your clock starts ticking.

✅ 5. Compare, Don’t Assume

Insurance ads love words like “comprehensive” and “affordable.” Ignore the hype.

- Always request the Table of Benefits.

- Check for sub-limits (e.g. “surgery capped at KES 100K” hidden inside a 2M inpatient plan).

- Compare 2–3 providers before you commit.

✅ 6. Keep It Alive — Never Miss a Payment

Even a one-week lapse can:

- Reset waiting periods.

- Deny your claims.

- Force you to reapply like a stranger.

Set reminders. Automate if you can. Treat premiums like rent — si kitu ya kuchezea.

Example: The 28-Year-Old Freelancer in Nairobi

- SHA (mandatory): KES 2,200/month (on 80K income).

- Budget Private Inpatient Plan (2M limit): ~KES 1,800/month.

👉 Total = ~KES 4,000/month.

But if your income is lower (say 30K/month), SHA is just KES 825/month, leaving room for a KES 1,500 private plan. That keeps you comfortably under KES 2,500/month.

Conclusion: Peace of Mind Doesn’t Need to Be Expensive

For less than the cost of two nights out in Nairobi, you can lock in medical cover that saves you from debt, stress, and WhatsApp harambees.

Your first plan won’t be flashy — but it’s your foundation. And foundations are what keep everything standing.

Ready to Get Started?

Get personalized advice and quotes tailored to your needs. No pressure, just honest guidance.

👉 Or start a chat with our assistant now.