The Freelancer's Survival Guide to Bulletproof Health Insurance in Kenya

Being a freelancer in Kenya is equal parts freedom and risk.

You set your own hours, choose your gigs, and send those invoices with pride. But there’s a dark side: no HR, no payslip deductions, no automatic health cover.

If you don’t sort your own medical insurance, hakuna mtu atakuchunga. And in this country, one accident, one illness, or one hospital deposit request can wipe out months — even years — of your hustle savings.

This guide is for you: the self-employed Kenyan carving your path outside the 8–5. Let’s build you a bulletproof health insurance plan that won’t collapse when you need it most.

Table of Contents

- Step 1: Face the Risk Like a CEO

- Step 2: Pick the Right Building Blocks

- Step 3: Budget Without Lying to Yourself

- Step 4: Don’t Get Caught by Lapses

- Step 5: Build a Broker into Your Team

- Case Study: Brian the Graphic Designer

- Final Word: Hustle is Freedom — Don’t Let Sickness Steal It

Step 1: Face the Risk Like a CEO

As a freelancer, you are your own HR. That means you have to audit your risks yourself.

Ask:

- How much can I handle out-of-pocket right now if I got into an accident?

- Do I have dependents — spouse, kids, parents — relying on me?

- Am I more concerned about big emergencies (inpatient) or everyday visits (outpatient)?

👉 Think of it this way: SHA (the old NHIF replacement) is your ugali — basic foundation. But for nyama choma (comfort, private hospitals, specialists), you’ll need to top up with private cover.

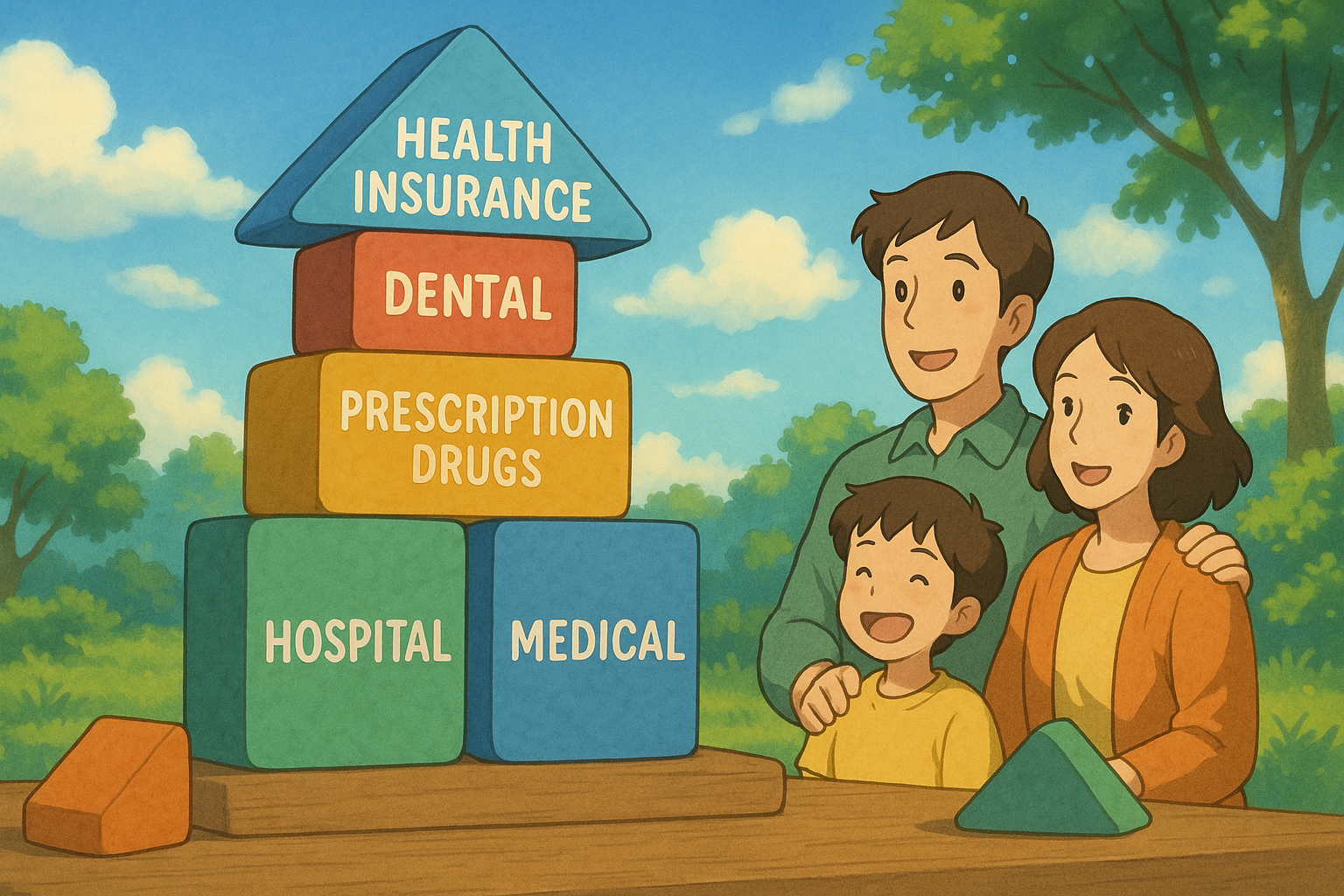

Step 2: Pick the Right Building Blocks

Freelancers don’t always have the cash for those glossy, all-inclusive “corporate” packages. So you build strategically.

The Must-Haves:

- Inpatient Cover → your parachute when things go really wrong.

- Outpatient Add-On → if you have kids, or if you fall sick often, this is a game changer.

- NHIF / SHA Compliance → treat that 2.75% deduction as non-negotiable. It’s your legal floor.

Smart Extras (if you can stretch):

- Maternity (for young families) → but remember the 10–12 month waiting period.

- Dental/Optical → useful for freelancers glued to laptops and late-night gigs.

- Last Expense / Funeral Cover → cheap but powerful family protection.

Step 3: Budget Without Lying to Yourself

Many freelancers fall into the affordability trap: choosing the cheapest plan to “just have something.”

But cheapest often means:

- Tiny hospital network.

- Sub-limits that won’t even cover surgery.

- Co-payments that feel like paying twice.

💡 Rule of thumb:

- Put aside 5–10% of your average monthly income for insurance.

- If your income fluctuates, budget based on your good months — and save a small cushion for lean times so your policy never lapses.

Step 4: Don’t Get Caught by Lapses

Remember James & Mercy’s story? (link internally to Lapsed and Lost post).

One missed renewal can mean:

- Fresh waiting periods.

- Declined claims.

- Or worse, zero cover when you need it most.

👉 Treat your premium like rent. Whether cash is flowing or not, it must be paid.

Set reminders. Automate with standing orders. Or ask your agent to call you before lapse — a good one will.

Step 5: Build a Broker into Your Team

Think of an independent broker as your outsourced HR. They:

- Compare different insurers (so you don’t drown in brochures).

- Warn you about hidden sub-limits.

- Chase the insurer when claims stall.

Freelancers already juggle a dozen things. Offload this headache.

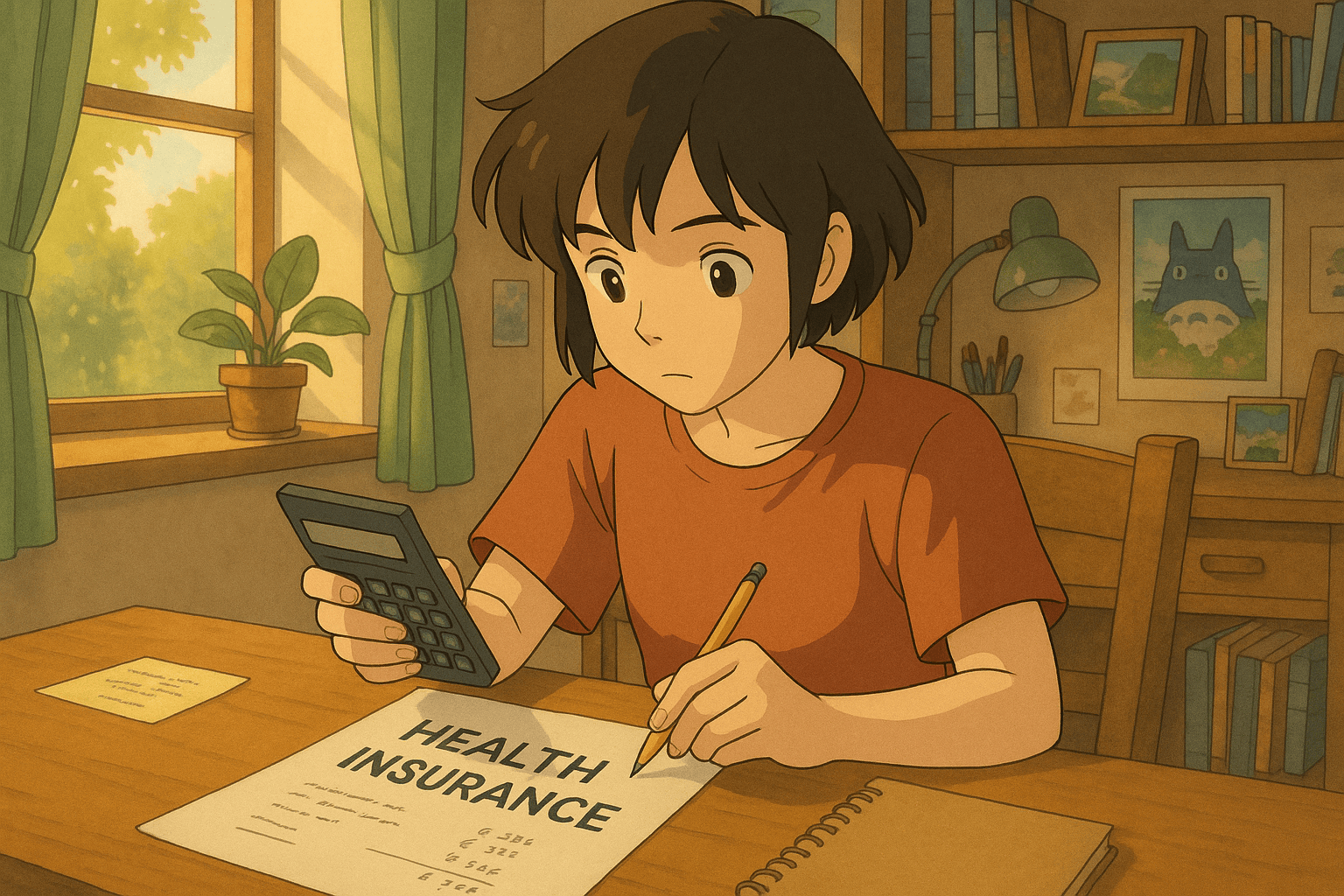

Case Study: Brian the Graphic Designer

Brian, 32, earns an average of KES 80,000/month from freelance gigs. Some months he makes 120K, others 40K.

His plan:

- SHA Contribution: ~KES 2,200/month (2.75%).

- Private Inpatient Cover: KES 3M limit (~KES 100K/year).

- Outpatient Add-On: KES 50K limit (~KES 40K/year).

His total yearly spend: KES 140K (about 12% of average income).

Result? He’s sorted. Whether it’s malaria, an accident, or a big emergency, Brian won’t have to sell his laptop or beg clients for “early payment.”

Final Word: Hustle is Freedom — Don’t Let Sickness Steal It

Freelancing in Kenya already comes with enough uncertainty.

Your health shouldn’t be one of them.

With the right mix of SHA compliance, smart private cover, and a bit of discipline, you can build a bulletproof health insurance plan that keeps you free to focus on your craft, your clients, and your dreams.

Because the only thing worse than missing a client deadline… is missing a hospital admission because you didn’t renew your cover.

Ready to Get Started?

Get personalized advice and quotes tailored to your needs. No pressure, just honest guidance.

👉 Or start a chat with our assistant now.